Wildfire Preparedness: The 48-Hour Documentation Window Before Evacuation

When wildfire is approaching, the window to capture what you own shrinks to hours. Here is the practical pre-evacuation documentation plan that insurance pays on.

By Matt Price

Founder & Builder, DwellRecord

Part of our insurance series: the full framework lives in The Complete Home Inventory Guide for Insurance Claims. This post covers the narrow window where good documentation becomes critical in hours, not weeks.

If you live in wildfire country — and in 2026 that's a steadily expanding geography across the American West, the Rocky Mountains, the Southeast, and even parts of the Great Plains — the hardest moment to do good documentation is exactly when you need it most. Smoke is visible on the ridge, the air smells like burning duff, and you're watching evacuation warnings roll through on your phone. The next 48 hours can make or break an insurance claim for a total loss.

The goal of this guide is simple: if you already have an inventory, use this to refresh it. If you don't, use this to build one fast enough to matter.

Why the 48-Hour Window Is Different

Every other kind of loss event — a burst pipe, a kitchen fire, a burglary — leaves the structure intact enough for you to document what happened after the fact. Wildfire total losses don't. The III's Facts + Statistics on homeowners insurance shows fire as the category with the lowest claim frequency but the highest average severity per claim. Wildfire specifically is a subset of fire where the loss is frequently total, the structure is fully consumed, and nothing remains to photograph except ash.

Which means: whatever documentation you have before you leave is the documentation an adjuster works from. There is no "after" to supplement it. Photos taken during evacuation, uploaded to the cloud, become the record of what you owned.

Phase 1: Before Fire Season Starts (Year-Round Preparation)

The best time to do wildfire documentation is six months before a fire is anywhere near you.

Build the Room-by-Room Inventory

See the home inventory checklist spoke for the full room-by-room approach. The short version for wildfire country:

- Every room, every closet, every cabinet

- Photographs of everything, including open drawers

- Serial numbers on appliances, electronics, power tools, firearms

- Values on anything over $500

- Appraisals on anything over $2,500 (see our scheduling guide)

Wildfire documentation especially rewards Tier 3 detail. Total losses are where the gap between "I know I had stuff worth $180,000" and "I can prove I had stuff worth $180,000" costs the most money.

Photograph the Structure

Not just belongings — the building itself:

- Every room from multiple angles

- Built-in features: custom cabinetry, wainscoting, fireplace surround, tile work

- Finishes: flooring type, wall colors, trim, hardware

- Exterior: siding, roof, landscaping, outbuildings

- Mechanical: HVAC units, water heater, panel box

If the structure burns, the claim rebuild is based on what the insurer's contractor scopes. Your photos are leverage to ensure the rebuild matches what you had, not a generic builder-grade version.

Store Documentation Off-Site

The most important rule in wildfire documentation: your records cannot live only in the home.

- Cloud-based inventory (Google Drive, Dropbox, iCloud, DwellRecord) — primary

- External hard drive at a family member's or office — backup

- Printed critical documents in a fire-rated safe inside the home — secondary only

A home inventory on a laptop that burns in the fire is worthless. A cloud-based inventory accessible from your phone at a hotel 200 miles away is the record the adjuster reads.

Meet Coverage to Actual Rebuild Cost

The Insurance Information Institute's coverage sizing guidance is a sanity check, but for wildfire country:

- Get an actual rebuild cost estimate from a local contractor (not Zillow value, not purchase price)

- Compare to your Coverage A dwelling limit

- Gap? Increase coverage, or add an Extended Replacement Cost or Guaranteed Replacement Cost endorsement

Rebuilding after a regional wildfire is dramatically more expensive than rebuilding one isolated home — labor and materials spike as thousands of claims hit the same area simultaneously. Extended coverage (125–150% of dwelling limit) is worth the small premium in fire-prone regions.

Check Policy Exclusions

Some policies in wildfire-prone states have started adding:

- Wildfire-specific deductibles (often percentage-based, 1-5% of dwelling limit)

- Brush removal / defensible space requirements as policy conditions

- Co-insurance clauses that penalize under-insurance

Read your policy renewal notice carefully. The conditions change.

Phase 2: Fire Weather Advisory — Days in Advance

When Red Flag warnings are issued or fires are reported anywhere in your region, move into preparation mode even if you're not under warning.

Refresh Your Inventory

- Walk every room with your phone camera. Ten-second pan per room.

- Open cabinets, closets, drawers you haven't documented recently

- Photograph any new items acquired since last inventory update

- Upload the new photos to cloud storage immediately

Gather Go-Bag Documents

If you have to evacuate on hours of notice, you want:

- Driver's license and passports (physical + phone photos of both sides)

- Social security cards or passport cards

- Birth certificates, marriage certificates

- Homeowners insurance declarations page + claim phone number

- Mortgage statements

- Vehicle titles and registration

- Photo of every room of your house (timestamped — see below)

- Emergency contact list on paper

- Cash (ATMs won't work in power outages)

Most of these live in a fire-safe at home. For hours-of-notice evacuation, make phone photos of every key document so they're in your cloud regardless of whether you can retrieve the physical documents.

Back Up Digital Records

- Photos from your phone — confirm cloud backup is current

- Computer files — confirm backup is current

- DwellRecord or whatever inventory system — force sync

If any of these rely on power or home Wi-Fi to sync, now is the moment to verify they're actually in the cloud.

Phase 3: Evacuation Warning (6-24 Hours)

When evacuation warnings (not yet orders) go out:

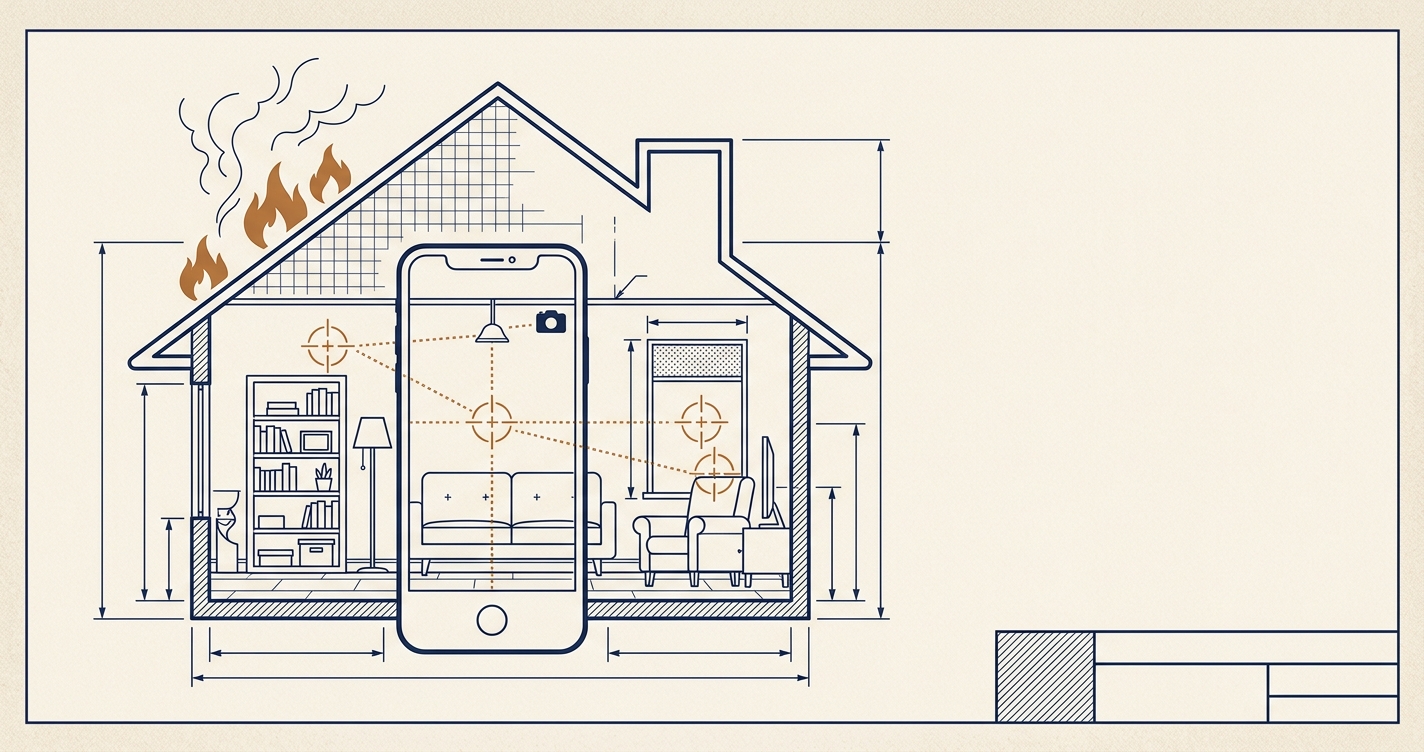

The 30-Minute Walkthrough

Take your phone. Walk every room of the house. Record video (more information than photos per second), narrating as you go:

- "Living room. Sofa, two armchairs, coffee table, TV (Samsung 65" QLED, wall-mounted). Rug. Bookshelf — these are first editions in the top row."

- "Primary bedroom. Bed, two nightstands, dresser. Dresser top drawer contains jewelry box. Closet: clothes, shoes, safe in back corner."

- "Kitchen. Refrigerator (Samsung French-door, bought 2023). Range, dishwasher, microwave. Cabinets contain standard kitchenware, plus the stand mixer, espresso machine, and wine fridge below the bar."

Narrate high-value items specifically. A 30-minute video with narration becomes a legal-quality document of what was in your home.

Photograph Specific High-Value Items

Beyond the walkthrough video:

- Every scheduled item (jewelry, art, watches) close-up

- Any irreplaceable sentimental items (family heirlooms, photo albums)

- Musical instruments, tools, collections individually

- Open safes to document contents (photo only — leave contents inside the safe)

Upload Immediately

Before you leave the structure:

- Confirm the walkthrough video is in the cloud (not just on your phone)

- Confirm photos are syncing

- Text a summary + key photos to a family member at a distant location

Phase 4: Evacuation Order (Hours or Less)

When evacuation becomes mandatory:

Take What Fits in the Vehicle

Priority:

- People and pets

- Medications

- Essential documents (go-bag from Phase 2)

- Laptops, external drives (if they don't slow you down)

- Irreplaceable items: family photos, heirloom jewelry, one-of-a-kind objects

- A few days of clothing

- Pet food, water, leashes, carriers

What not to take:

- Things you have insurance for

- Things that will slow the vehicle or make it unsafe

- Things that will cause you to delay departure

The insurance is for everything in category one. Your documentation is for everything you left.

Final Photo Sweep

If time allows — and only if:

- Photograph the exterior of the house from multiple angles

- Photograph the immediate surroundings (neighbors, landmarks)

- Time-stamp the evacuation start on any remaining documentation

Leave

Evacuation orders exist because staying is genuinely dangerous. Every year, people die waiting to save objects. The objects are replaceable. You aren't.

Phase 5: During the Event

Once you're evacuated to a safe location:

Contact Your Insurer

Call the 24-hour claim line the moment the evacuation is over. Open a precautionary claim file. You don't need to know the outcome yet — you're starting the record.

Get a claim number even if no damage has occurred. Establishing an early timeline is protective.

Track Expenses

From the moment you evacuate, Coverage D (Loss of Use / Additional Living Expenses) is potentially in play. Keep every receipt:

- Hotel, Airbnb, temporary rental

- Meals out (above what you'd normally spend on groceries)

- Laundry, toiletries, clothing

- Pet boarding

- Additional mileage if driving to work or school from temporary housing

- Phone/internet service in the new location

This reimbursement often surprises homeowners by how much it covers. Track everything. See our claim filing guide for the full ALE process.

Monitor Official Sources Only

Neighbors and social media will be wrong in both directions. Check:

- Local sheriff's emergency alerts

- Cal Fire (or your state fire authority) incident reports

- County emergency management pages

- InciWeb for federal incidents

Do not return to the area until authorities explicitly permit it.

Phase 6: After the Fire

When re-entry is authorized:

Do Not Touch Anything Before Photographing

Same rule as any claim: photograph and video every inch of damage before cleanup. But with wildfire, there often isn't much to photograph except ash and foundation. Photograph that too — the scope of destruction is the claim.

Walk the Property With the Adjuster

When the field adjuster arrives:

- Provide your pre-evacuation walkthrough video

- Provide your full home inventory PDF

- Provide all scheduled-item appraisals

- Walk the debris field with them

- Photograph their inspection

Don't Rush to Clean Up

Some insurers require their approved environmental remediation before debris removal (asbestos, lead paint, other hazards present in older homes after fires). Rushing cleanup can forfeit coverage. Wait for the insurer's process.

Engage Professionals Early

For total-loss wildfire claims, a public adjuster is often worth their 10-15% fee. The documentation density, rebuild-cost negotiations, and potential underinsurance issues benefit from representation.

The Documentation Systems That Actually Work Under Pressure

Wildfire exposes every weakness in home documentation:

- Shoebox of receipts in the home — gone

- Spreadsheet on the laptop you left behind — gone

- Photos on phone only, not in cloud — gone if phone is lost or reset

- Cloud photos with no organization — exists but takes weeks to sort through under stress

What works:

- Cloud-synced inventory app with structured data and photos per room — export to PDF in minutes at claim time

- 30-minute narrated walkthrough video uploaded before evacuation — legal-quality documentation of contents

- Appraisals for scheduled items stored in cloud alongside inventory

- Pre-existing ALE awareness — you start tracking expenses from hour one instead of week three

DwellRecord was built specifically for this pattern. Room-by-room inventory with photos, serial numbers, values, and receipts — synced to the cloud automatically so it survives the event that requires it. When you need it, export a single PDF that covers every room, every item, every appraisal. Create your free account before the season where you need it.

Frequently Asked Questions

How much notice does a wildfire usually give?It varies dramatically. Some fires give 3–5 days of warning as they approach. Others give under an hour. Plan for the worst case and you're always ready.

Does standard homeowners insurance cover wildfire?Fire is a covered peril under standard HO-3 policies. The complications are underinsurance (your Coverage A limit isn't enough to actually rebuild at post-disaster prices) and specific wildfire deductibles in some high-risk states.

What about non-insured properties in high-risk areas?Some California, Oregon, and Colorado insurers have reduced or withdrawn coverage in certain areas. California's FAIR Plan is a last-resort option. Check availability annually — the market changes fast.

Should I have a specific "wildfire evacuation" policy?Your homeowners policy covers wildfire. What's often needed is supplemental coverage: extended replacement cost, building ordinance/law coverage, and sometimes a separate flood policy for post-fire debris flows.

What if I rent?Renters insurance works the same way for contents. The structure is the landlord's problem. Your belongings, photos, and documentation are yours. Build the same inventory.

Related Guides

- The Complete Home Inventory Guide for Insurance Claims — cluster hub.

- Home Inventory Checklist for Insurance Claims — room-by-room documentation.

- Scheduling Jewelry, Art, and High-Value Items — for the items standard policies sub-limit.

- RCV vs. ACV — the settlement method that determines how much depreciation the insurer takes off the top.

- How to File a Homeowners Insurance Claim — the step-by-step playbook after a loss.

The Bottom Line

Wildfire doesn't give you a second chance to document. The photos you take before you leave become the record an adjuster works from. Build the inventory now. Keep it in the cloud. Refresh it annually — and more seriously the moment Red Flag warnings enter your region. And when the order comes to evacuate, take your people and the items you truly cannot replace, and trust that everything else is on the list you already made.

Editorial, not advice. This article is educational and reflects publicly available IRS, state, and insurance guidance at the time of writing. It is not tax, legal, or insurance advice. For decisions that touch your specific situation, consult a CPA, enrolled agent, tax attorney, or licensed insurance professional in your state. DwellRecord keeps the record — your advisor makes the call.

Last reviewed:

Ready to protect your home investment?

Start documenting your improvements, assets, and warranties for free.

Get Started Free